How To Create A Debt Repayment Plan

Paying off debt can feel overwhelming if you don’t have a plan in place. After going through financial ups and downs myself, I know that breaking it down into manageable steps really makes everything easier. Creating a debt repayment plan not only puts you in control but also helps you clearly see where your money is going and how to prioritize what you pay off first. If you’re starting out, knowing where to begin is sometimes the hardest part, but a practical plan can help you make real progress toward becoming debt-free.

Why Creating a Debt Repayment Plan Matters

When I struggled with credit card balances and a car loan, I stumbled upon the fact that having a proper repayment plan gave me more visibility over my finances and let me make decisions with confidence. Many people carry multiple debts at once, which can lead to missed payments, growing interest charges, and unnecessary stress. Without a structured approach, it’s easy to simply pay the minimum and feel like you’re getting nowhere.

Setting up a plan helps you organize your debts, know exactly how much you owe and to whom, and helps you pay off what you can afford each month. According to the Federal Reserve, consumer debt continues to rise, which means a lot of people are facing similar challenges. Getting a handle on it can free up money for savings and the things that matter most to you.

If you’re looking to build healthy financial habits, setting a realistic debt repayment plan should be your first step toward regaining control.

You can also click here for more personal finance tips.

Getting Started: Understanding Your Debt

I found that the first step in creating any plan is understanding exactly what you owe. That means gathering all your account information and putting it in one place so you have the full picture.

- List Every Debt: Write down every debt you owe, including credit cards, student loans, car loans, payday loans, or personal loans. Include the total balance, minimum monthly payment, due date, and interest rate.

- Total Everything Up: Add up your balances to see your starting point. Sometimes, just seeing the number can be a wake-up call, but it gives you a clear goal to work towards.

- Check Interest Rates: Interest rates are really important. High-interest debts cost you more money over time, so knowing these rates helps you decide which debts to prioritize.

You can grab a simple spreadsheet or use a debt repayment app to keep track. I’ve found it easier to update digitally, but pen and paper also works just as well. Taking this step gives you a feeling of control and clarity right from the start.

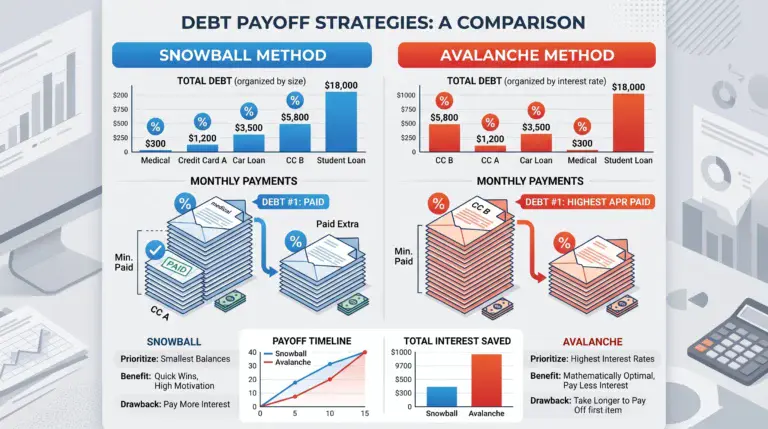

Common Debt Repayment Methods

After understanding my debts, the next step I took was choosing a way to pay them down. Here are the two most popular approaches that financial advisors usually recommend:

- Snowball Method: You pay off your smallest debt first while making minimum payments on the rest. Once the smallest is paid, you roll its payment into the next-smallest debt. It’s great for building motivation because you see quick wins early on. There’s a full breakdown of the snowball approach in my article on debt snowball vs avalanche methods.

- Avalanche Method: You pay off the debt with the highest interest rate first, which saves you money in the long run. This method is a bit slower when it comes to checking debts off your list, but it reduces the total interest paid. For the math-minded, this option often makes more sense.

I started with the snowball method, because those early successes kept me involved. If your main motivation is saving the most on interest, avalanche may work better for you. Some people blend different methods if it makes things easier to stick with, so choose what fits you best.

Building Your Own Debt Repayment Plan

Customizing your plan to fit your life has the best longterm results. Here’s how I break it down step by step:

- Prioritize Debts: Decide which method you want to follow, snowball, avalanche, or even a custom mix. But unless you have medical debt, I would recommend putting credit cards first because of the way credit cards calculate interest.

- Create a Budget: Look at your monthly income and expenses. Figure out how much extra you can realistically put toward debt payments after covering essentials like rent, utilities, food, and transportation. For tips, check out my guide on how to create a realistic budget.

- Allocate Payments: Make at least minimum payments on all your debts to keep your accounts in good standing and avoid fees. Then, put any extra money toward the one debt you want to tackle first.

- Automate Payments: Automating as much as possible helps you avoid late fees and keeps you consistent. Many banks let you set up automatic payments for both minimums and extra payments.

- Adjust and Track: Review your progress each month. If you get a bonus, tax refund, or extra income, put some (or all) of it toward debt. Track your payments so you can see your balances drop over time; it’s motivating!

Sharing your goal with a friend or family member, or joining a community like those found on personal finance forums, can keep you accountable and motivated. If you prefer working with a professional, a certified credit counselor can help customize a plan for you.

Factors to Think About Before Starting Your Plan

Planning out your debt repayment works best if you consider potential challenges and make room for flexibility. Here are a few things I encountered along the way:

- Emergency Fund: Having a small emergency fund (at least $500–$1,000) can keep you from adding to your debt if surprises come up. If your car breaks down or you have a medical bill, you won’t need to swipe a credit card.

- Income Fluctuations: If you have variable income, plan your minimum payments conservatively. Use higher-earning months to pay extra, but keep things manageable during leaner times.

- Debt Consolidation: Combining several debts into one loan or card with a lower interest rate can simplify your repayment strategy. I wrote about the pros and cons of this in the debt consolidation guide on this site. Some people find consolidation makes tracking easier and reduces the total number of bills.

- Balance Transfer Offers: Some credit cards let you transfer balances and pay 0% interest for a set period. This can save you money, but read the fine print about fees and the interest rate after the intro period. Be sure to finish paying off the amount before the higher rate kicks in.

- Avoid Accumulating New Debt: Pausing big purchases and putting new charges on hold while you work on repayment is really important. Otherwise, you end up undoing all the progress you’ve made. Cutting back temporarily can help you build positive momentum.

Building an Emergency Fund While Repaying Debt

You might wonder if it makes sense to save while you’re paying down debt. From my experience, having even a small cushion has made a huge difference in staying out of the debt cycle. There’s more on this topic in my post about how much you should save for an emergency fund. Setting aside even $20 a month for emergencies can prevent setbacks that would otherwise put you deeper in debt.

Advanced Tips as You Gain Momentum

Once you’ve built momentum, these strategies can give a boost to your progress and help you pay off debt even faster:

Refinancing Loans: If you qualify, refinancing at a lower interest rate can reduce payments or shorten the repayment period. This is common with auto loans and some student loans. Check out how to refinance student loans for a step-by-step guide. Always read the terms before you sign anything.

Increase Your Income: Picking up a side hustle, freelancing, or selling items you no longer need can provide extra cash to put toward debts. Small amounts add up over time and can speed things up. You could even consider asking for a raise at work; even a little extra goes a long way.

Negotiate Rates or Settlements: Some creditors may be willing to reduce your interest rate or work out a settlement. This can make a big difference if you’re feeling stuck. For more on how to handle debt collections, see my article about dealing with debt collectors. Just be aware, settlements can have credit score and tax impacts, so look over all the pros and cons.

Reward Yourself: Setting small milestones and giving yourself a budget-friendly reward keeps you motivated. Something simple like a favorite treat or a free activity helps you celebrate your efforts. Choose non-spending rewards to keep yourself motivated without breaking your budget.

Debt Repayment Plan FAQ

Here are some questions I often get from people who are just starting to get serious about paying off debt:

Question: Should I pay off the smallest debt first or the highest interest one?

Answer: That’s up to you. The snowball method works well for building motivation, while the avalanche method helps you save more on interest. Choose what fits your personality and needs.

Question: How do I stay motivated when progress feels slow?

Answer: Tracking your progress visually, like a chart or checklist, makes your efforts real. Join online support groups, share your goal with a friend, or set up a reward system to celebrate small wins. Keeping things visual can make a surprisingly big difference.

Question: What if I get stuck and can’t make a payment?

Answer: Reach out to your creditors before missing a payment. They might offer hardship plans or help you set up smaller, temporary payments. For more help, a credit counselor can talk you through next steps.

Kickstarting Your Debt-Free Adventure

Creating a debt repayment plan doesn’t have to be intimidating. By getting organized, choosing the repayment approach that fits best, and making adjustments when life happens, I’ve gained more control over my future and less stress over money. Getting started is the toughest part, but every payment brings you closer to financial freedom. Stay patient, keep adjusting your plan as your life changes, and remember there are lots of resources and communities to support you along the way. Make your next move today—even if it’s just listing out your debts, it’s a step forward on your own path to a debt-free life.