10 Steps To Building A Budget That Actually Works

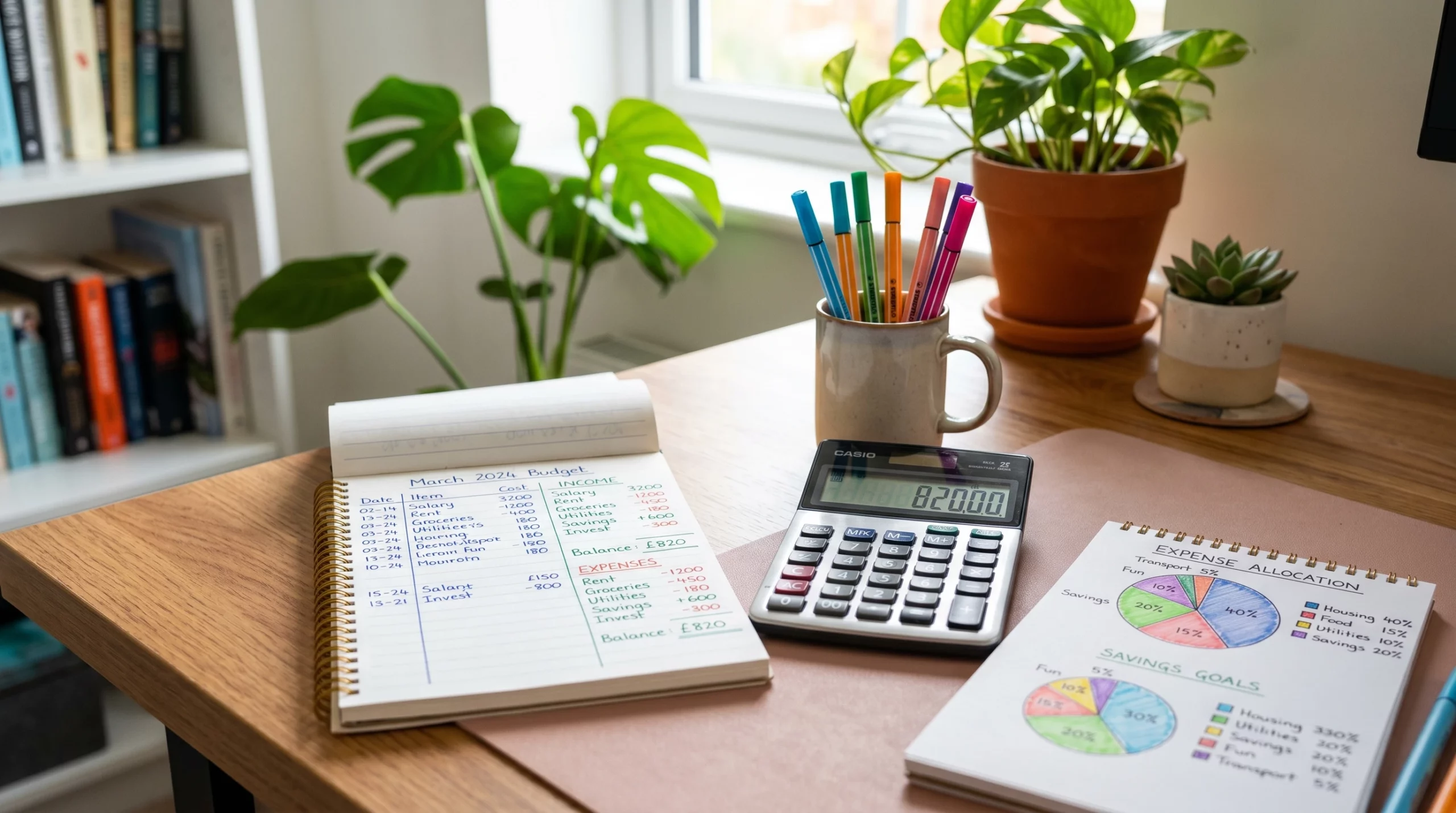

Building a monthly budget might sound overwhelming if you’ve never done it before. But it doesn’t have to be complicated. I’ve found that setting up a system makes it easier to see where your money is coming from, where it is going, and how you can reach your savings goals, at any time.

Building a monthly budget might sound overwhelming if you’ve never done it before. But it doesn’t have to be complicated. I’ve found that setting up a system makes it easier to see where your money is coming from, where it is going, and how you can reach your savings goals, at any time.

Budgeting is not about micromanaging every cent. It is about knowing your habits, making smarter choices, and having money left over for both your needs and the things that make life fun. I am sharing my 10-step process below. Once you go through these steps, you’ll have a budget blueprint you can actually stick to and tweak as your situation changes.

Step 1: Figure Out Why You Want a Budget

Before getting into the numbers, I like to get clear on the reason behind budgeting. Everyone’s motivation is different. Maybe you want to pay off debt, save for a vacation, build an emergency fund, or just stop overdrafting your checking account. Your “why” can help you stay motivated on days you’d rather skip tracking your spending.

Brainstorm Your Main Goals

- Do you want to stop living paycheck to paycheck?

- Are there things you want to save for, like a car, home, or trip?

- Would you like to reduce debt or build an emergency cushion?

- Is there a certain amount you want to save every month?

Write down your reasons and keep your goals where you can see them. Seeing your “why” makes sticking to a budget easier in the long run. When times get tough (and they will), reviewing your ‘why’ can boost your resolve.

Step 2: List Your Take-Home Income

I always start by figuring out how much money I will have available each month after taxes, insurance, and other deductions. Check your pay stubs, bank deposits, or invoices if you’re self employed. Do not forget any side gig earnings, government payments, child support, or other cash that comes in each month.

Tips for Tallying Income

- Use net (after-tax) income

- Include all consistent sources

- For variable pay, use a three month rolling average of the last three months.

Knowing your true monthly incometells you how many dollors you have to work with for that month. If you have additional income throughout the year, such as bonuses or irregular freelance work, consider how these can support your overall money goals.

Step 3: Track Your Spending for a Month

This part takes effort, but You have to do it. Tracking your expenses checking bank statements or using an expense tracker app gives you a real picture of your current spending habits. Even tracking for just 30 days can show patterns that surprise you.

What to Include

- Rent or mortgage

- Utilities (electric, water, internet, etc.)

- Groceries and eating out

- Transportation (car payments, gas, public transit)

- Subscription services

- All other spending; no detail is too small

You should not judge judge your past choices. Just get all the data-and that’s all it is…data. Once you have one month’s worth of data, you can spot where little things add up and pick out areas ripe for change.

Step 4: Categorize Your Expenses

I find it easiest to break expenses into clear categories. Common ones include housing, utilities, food, transportation, debt payments, savings, entertainment, and personal care.

Sorting expenses into buckets helps you better understand where your money’s actually going each month and where you might want to change your habits.

Simple Budget Categories

- Needs: rent, bills, groceries, minimum loan payments

- Wants: dining out, streaming, hobbies, shopping

- Savings/Debt: emergency fund, longterm goals, extra debt payments

Some people prefer more categories or fewer. Do what works best for you. Just keep your categories consistent for easy tracking and to have a better sense of your spending.

Step 5: Add Up All Your Monthly Expenses

Add up what you spend in each category every month. Use the averages from the past one to three months for expenses that are not exact or that fluctuate throughout the year.

This also helps when budgeting for expenses like annual subscription fees or gifts; break those amounts down so you spread them across all months.

Include Everything

- Monthly totals for each main category

- Any irregular or yearly expenses (averaged out monthly)

- Emergency or oneoff costs (if you have them)

Adding up your expenses is often the biggest eyeopener. Sometimes spending on eating out or subscription services is much higher than you guessed. That’s why tracking is so helpful—it shows you where small changes can help you keep more cash each month.

Step 6: Compare Income and Expenses

Subtract your total monthly expenses from your take-home income to see if you are positive or negative. If you are spending less than you earn, awesome. You have money to put toward savings or debt. If you are spending more, there is room to adjust before things get stressful.

What If There’s a Gap?

- If spending is greater than income: Find areas to trim back such as subscriptions, takeout, or impulse buys

- If income is greater than spending: Decide how extra cash can help you reach your goals (save more, pay debt, invest)

This quick check shows if your budget needs an unused subscription service dropped or a bigger overhaul. If necessary, come up with different budgets for leaner months and better months than the base case as well.

Step 7: Set Spending Limits for Each Category

Decide how much you’ll spend on each main category. For essentials like rent or utilities, there is often not much wiggle room, but things like dining out, entertainment, or online shopping offer more flexibility. Base these numbers on what you have been spending, but change them to match your savings and financial goals. Setting clear limits makes it easier to hold yourself accountable, and lets you move money between categories as needed.

Budgeting Rules Worth Noting

- The 50/30/20 Rule: 50% to needs, 30% to wants, 20% to savings/debt

- ZeroBased Budgeting: Give every dollar a job

You can mix and match approaches. The real goal is to keep spending within your income and give yourself a roadmap for the month ahead. If you need to, start small and adjust as you see what works.

Step 8: Pick Your Budgeting Tools

I am a big fan of simple solutions. You could use a spreadsheet, a pen and notepad, or one of the many free budget apps available. Some banks even have really good built-in trackers. The best tool is the one you will stick with, so don’t overcomplicate it.

Popular Options

- Spreadsheets (Google Sheets, Excel)

- Budget apps (YNAB, Mint, Goodbudget)

- Printable trackers (for those who prefer pen and paper)

Anything that keeps your goals and numbers in the same place will work. Try a few and see what feels easiest. And don’t be afraid to switch if your first choice does not work.

Step 9: Review, Adjust, and Check In Weekly

I check my budget at least once a week to make sure I am on track. Life throws curveballs. Maybe you get a big bill in the mail or you get a nice bonus. Small adjustments keep your budget realistic. If you overspend in one category, try to balance the overspend in another, or look for ways to cut back the next week.

Tips for Staying On Track

- Set a weekly reminder to check the budget

- Celebrate small wins, like making a savings goal or paying off a bill

- Do not forget to update spending if something changes

Budgeting is an ongoing process. reviewing your budget at least weekly really helps you stay motivated and avoid surprises. Share your progress with a friend for more accountability.

Step 10: Plan for Fun and Flexibility

Budgeting does not mean cutting out everything you love. I always make space for treats, hobbies, small luxuries, or whatever makes me smile. I recommend you do the same.

Life happens, so building in some flexibility makes your budget much easier to stick to over time. Allowing for flexibility also helps you stay positive about your finances and avoid feeling deprived.

Flexible Budgeting Ideas

- Set a fun money category that’s guilt-free

- Break yearly bills into monthly mini payments to avoid money stress

- Give yourself permission to adjust as life changes

The best budget is the one you’ll follow no matter what, so make it fit your real life, not just your ideal life.

Questions and Quick Fixes

What if my income changes every month?

Use your lowest average monthly income as your baseline, and set aside any extra as a buffer for slower months. This tactic helps smooth out the variability and gives you peace of mind when work or payments are unpredictable.

I can’t ever seem to stick to a budget; any tips?

- Start with tracking, not cutting. See where your cash goes, then adjust.

- Automate savings if you can.

- It’s okay to reset and try again. Progress counts more than perfection

Do I need to use cash envelopes?

Cash envelopes work for some people, but digital tools (or a mix) are just fine if you use other forms of payment. The main idea is to set limits and check in regularly. Try what feels natural and be patient with yourself as you find your groove.

Practical Next Steps

A simple monthly budget gives you more control, less stress, and a clearer path to your money goals. Here’s a quick and realistic plan you can try:

- Write down your monthly income and track your spending for two weeks.

- Sort your expenses into needs, wants, and savings/debt.

- Pick a budget tool and check your spending progress weekly.

What is the first thing you want a budget to help you with? Share your game plan below. I would love to hear how you are starting out, and remember: budgeting is a skill you build over time, not a finish line you cross in one try. Stay curious, and keep showing up for your future self!