The 50/30/20 Rule: Budgeting Made Easy

Managing money can feel confusing, but finding the right system can make budgeting feel less intimidating and way more doable. I’ve seen the 50/30/20 Rule help a lot of people, especially anyone new to tracking their personal finances. This simple percentage-based method helps organize spending and saving without the need for a complicated spreadsheet. Here I’ll walk through how it works, why it’s popular, how to use it, and practical tips I’ve picked up through my own experience using the 50/30/20 Rule.

Origins and Foundations of the 50/30/20 Rule

The 50/30/20 Rule was popularized by Elizabeth Warren, a U.S. Senator and bankruptcy law expert, along with her daughter Amelia Warren Tyagi. They introduced it in their influential 2005 book, “All Your Worth: The Ultimate Lifetime Money Plan.” Their big idea was to give people a straightforward way to manage their after-tax income, splitting it into just three buckets, rather than juggling endless subcategories. This concept caught on because you don’t need to be a financial expert to try it. I’ve found that it can work really well as a starter template. The appeal lies in its simplicity, helping those who may have bounced between multiple budgeting methods settle into a sustainable structure that doesn’t require constant recalculations.

Breaking Down the Three Categories

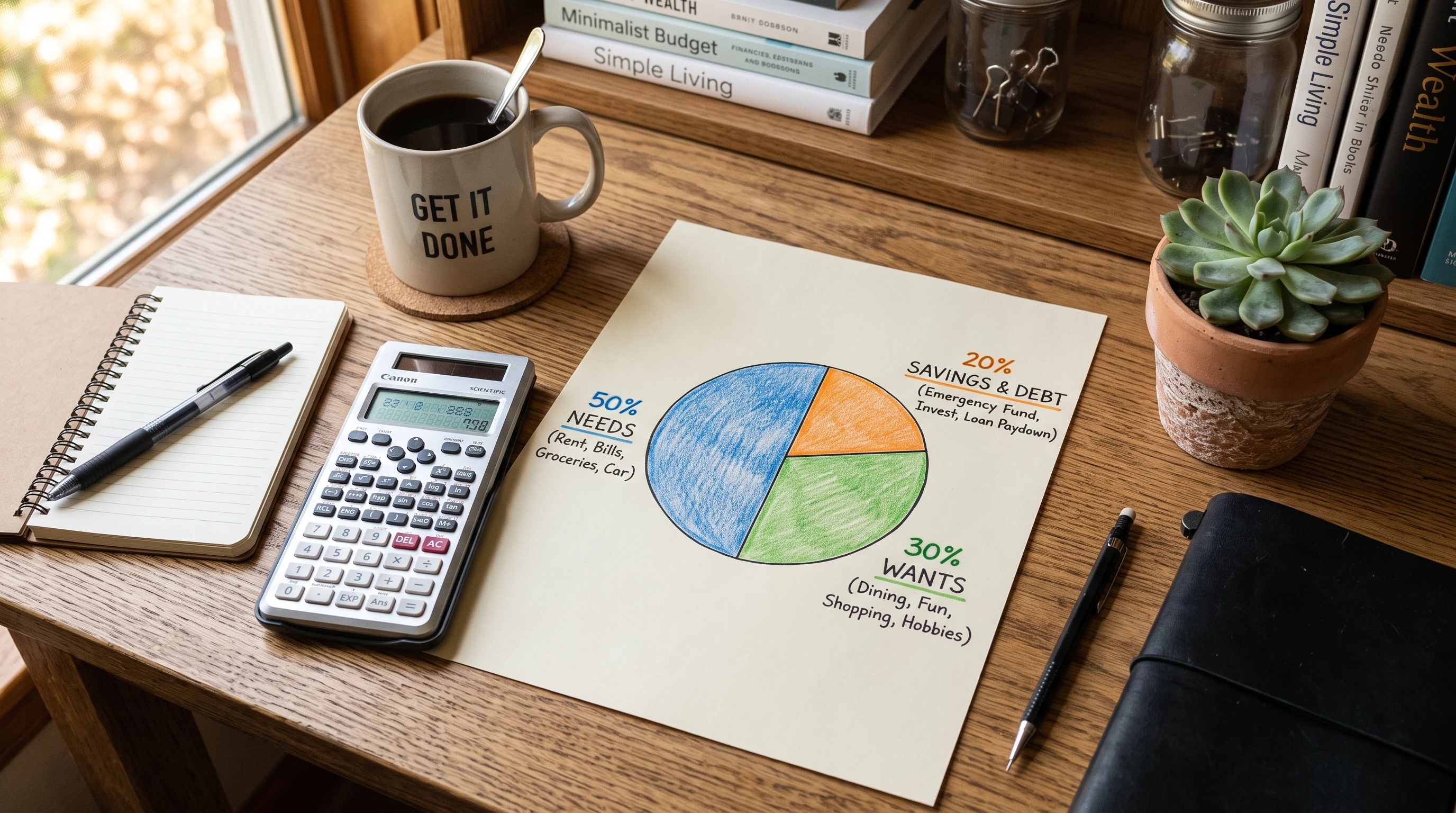

Following the 50/30/20 Rule, I take my monthly after-tax (takehome) pay and divide it into three types of spending: needs, wants, and savings/financial goals. Here’s what each one means:

- 50% for Needs: These are the basics that I can’t really cut out. That includes mortgage or rent, utilities, essential groceries, transportation to work or school, required insurance (like health or auto), healthcare, childcare, and minimum required payments on debts. If I miss these, it can put my wellbeing or credit at risk.

- 30% for Wants: This bucket gives breathing room for things that make life more fun or comfortable, but aren’t strictly necessary. My wants are things like dining out, streaming services, entertainment, travel, nice-to-have tech, shopping, hobbies, and experiences like concerts or vacations.

- 20% for Savings & Financial Goals: Everything in this category is about planning for the future or improving financial security. This includes building up an emergency fund, making extra payments on debt, investing for retirement (like IRAs or 401(k)s), saving for a home, or setting aside money for big future expenses. If I want to get ahead financially, this bucket is the one that matters most over the long run.

While it might seem simple to split expenses in just three categories, sometimes you must double-check your spending to be sure you’re really counting needs and wants correctly. I often use my previous bank statements to get a read on what actually goes where, uncovering little recurring charges that belong in “wants” and must-pay expenses that fit better in “needs.”

Why the 50/30/20 Rule Makes Budgeting Easier

Budgeting with percentages cuts out the overwhelm. Instead of getting lost in dozens of expense categories every month, I just track what I’m spending in these three major groups. This makes it less likely that budgeting turns into a chore I want to avoid. Even if the numbers aren’t perfect, I can quickly check whether I’m close and make changes if I’m getting out of balance. By focusing on just these core parts, I’ve found that budgeting feels less restrictive and more about making intentional choices with money rather than simply restricting myself.

Benefits of the 50/30/20 Rule

- It’s easy to remember: The three-number split is simple, so I don’t get lost in details.

- Beginner friendly: Anyone can try it without needing hours of setup. There’s no special knowledge required.

- Flexible: The big categories can be tweaked as my life changes, like after moving, changing jobs, or having kids.

- Puts savings first: By making savings a set number from the start, I’m less likely to forget this super important step.

- Helps prevent lifestyle creep: As my income increases, so does the savings bucket, so it’s easier to build wealth without spending everything I earn.

- Supports long-term habits: Using these categories consistently makes me more mindful of my spending, which pays off over time. It’s amazing how a simple strategy, when repeated, can help instill long-lasting habits that support financial wellness.

Common Limitations and Criticisms

Even though the 50/30/20 Rule works well for many, it’s not perfect for every situation. Here are a few points that people sometimes bring up:

- High-cost housing areas: If I live in a city where rent or mortgages take up most of my income, the “50% for needs” rule can feel impossible.

- Lower-income households: When income is low, needs can easily use up more than 50%, making it really tough to stick to the suggested split, especially for families.

- High earners: For people with much higher income, following just 20% for saving might limit how much financial progress they can make. They could realistically save a lot more.

- It’s a starting point: The rule works best as a guideline. My financial goals, obligations, or where I live might mean I need to adjust the percentages to fit real life.

Additionally, in some cases, you might want to split out special categories like medical costs, unique work expenses, or ongoing education, placing them where they make the most sense for your lifestyle.

Needs vs. Wants: The Gray Areas

Sometimes people wonder what counts as a true need. I’ve realized that minimum monthly payments on debts (like credit cards or car loans) should always count in the needs category, since those are required to stay current. But if I pay extra each month to pay down the principal faster, that extra payment should come out of the 20% savings and financial goals portion. This keeps savings and debt reduction moving together.

There are definitely instances when you have to use your own judgment, especially for things like cell phone plans, internet upgrades, or improved car insurance. The key is to be honest about which expenses really keep life running and which simply make things a bit nicer. Drawing the line might seem tough at first, but over time, it becomes more apparent as you check in with your budget and reassess your spending habits.

How to Use the 20% Savings & Financial Goals Bucket

The real strength of the 50/30/20 Rule is how it encourages making progress toward major financial goals. Here’s how I like to think about my priorities for the 20% category:

- First, build an emergency fund: I aim for three to six months’ worth of essential expenses saved in cash. This is the safety net I fall back on when things go wrong. A job loss, car repair, or medical bill can happen without warning, and an emergency fund is what keeps it from turning into a bigger crisis.

- Next, pay off high-interest debt: After covering the minimums from the needs bucket, using this 20% chunk to knock out credit card balances or other expensive debt can be one of the best money moves there is. The relief from escaping high interest charges adds up over the years.

- Invest for retirement: Once debt is manageable, I start putting money into retirement accounts, including a 401(k), IRA, or an employer pension plan. Even small contributions make a big difference over time by letting compound growth work its magic.

- Save for long-term goals: Once I’m on track above, it’s nice to plan for other dreams, like a house down payment, a family vacation, or building wealth with taxable investments.

As you watch your savings grow, it can be motivating to set an annual challenge or mix in some new goals. For example, you might aim to increase your emergency fund by $1,000 this year or put a bit extra into a retirement account. Checking off milestones, even small ones, helps keep you engaged and reminds you that steady progress always counts.

Variations and Customizing the Rule

No budget method works for everyone. Sometimes I see people adjust the percentages to fit their lives, especially if they have unique goals or live somewhere with very high housing costs. Some examples are:

- 60/20/20: Needs take up a little more, wants and savings stay the same.

- 40/30/30: Wants drop, but savings get a real boost.

- Custom percentages: People might set up categories like 35/35/30, or anything that feels sustainable long-term. The core idea is still dividing income by type of spending, not by every possible bill. In reality, the best percentages are the ones you can stick to month after month.

As your financial situation changes, especially with big life transitions like marriage, children, or relocation, don’t hesitate to tweak your percentages. Sometimes even moving 5% from wants to savings can make a noticeable difference in your long-term financial picture.

Practical Tips for Getting Started

- Automate savings: I find it really helps to set up an automatic transfer right when my paycheck arrives so money goes to savings before I can spend it.

- Track and review regularly: Monthly or quarterly check-ins help me see if I’m keeping on track or slipping into old habits (like letting wants take over the needs category).

- Adjust as life changes: New job, new baby, moving cities; when big changes happen, I take a fresh look at my percentages.

- Bump up savings after raises: Instead of letting all raises go to lifestyle upgrades, I try to save a bigger piece. This “pay yourself first” mindset really adds up over time.

- Watch “wants” spending: It’s easy to lose track of things like small subscriptions or eating out a little too often. I try to be honest about what I’m choosing and check if some “wants” can be trimmed without sacrificing fun.

Staying consistent with your system, even when it requires discipline, delivers the biggest results. Find an approach you can enjoy and sustain—streamlining a process that works is better than aiming for a perfect but stressful budget.

Simple Example: Budgeting with $5,000 Takehome Income

If I bring home $5,000 a month after taxes, here’s what a 50/30/20 split would look like:

- Needs: $2,500 (housing, car, groceries, insurance, utilities)

- Wants: $1,500 (entertainment, dining, shopping, some travel)

- Savings & Financial Goals: $1,000 (building my emergency fund, paying extra toward debt, investing or saving for a house)

For many, this breakdown helps avoid overcomplicating things. You can do the math once—then use those target amounts to guide spending decisions all month long, checking in weekly or twice a month to see how you’re doing. Apps and online tools can also make it easy to track each category without old-school pencil-and-paper checklists.

The Compounding Path Perspective: Start Here, But Don’t Stop

The 50/30/20 Rule is a great launchpad for anyone wanting to get money under control, but it’s not the endpoint. Once income grows and debt shrinks, try to slowly push more into savings and investing if it can be managed, gradually moving to a split like 45/25/30 or even 40/20/40. The more is save and invest, the more money works through compounding, making future choices easier and giving a real sense of accomplishment.

The real key with any budgeting method is momentum. Consistency counts more than getting the numbers perfect every month. By sticking with a system—even if it’s not always pretty—I’ve learned to make money decisions with less stress and more confidence.

For more tips on creating a budget, check out our article on the steps to creating a budget here.

And finally, If you have questions or want to share how the 50/30/20 Rule works for you, drop a comment below! Your story or insight could make a difference for someone else starting their own budgeting adventure.