Understanding Credit Card Interest Rates

Understanding how credit card interest rates work is really important for managing my money wisely and staying out of unnecessary debt. When I first started using credit cards, the idea of interest seemed confusing, but once I broke it down, things started making a lot more sense. If you want to use credit cards without getting trapped by growing balances, knowing the details about interest rates and how credit card companies calculate fees can make a big difference.

What Credit Card Interest Is and How APR Works

Credit card interest is the amount I pay to borrow money from a credit card issuer. Every time I don’t pay off my full statement balance by the due date, I start to accrue interest on the remaining balance. It’s basically the cost of carrying a balance on my card, and these charges can add up surprisingly fast.

Credit card interest is typically expressed as an Annual Percentage Rate, or APR. This is a yearly interest rate that helps me compare the cost of borrowing between credit cards or different types of loans. Even though the APR is annualized, interest isn’t charged just once per year. Banks break it down to daily or monthly rates, so the balance can grow each day I don’t pay it off in full.

Different Types of APR: Purchase, Balance Transfer, Cash Advance, Penalty

Not all credit card charges use the same APR. Most cards use multiple rates, depending on the transaction.

- Purchase APR: This is the interest rate applied to my everyday credit card purchases when I don’t pay the balance in full.

- Balance Transfer APR: When I move a balance from one card to another, this rate applies to that transferred debt. Sometimes, there are special low introductory offers, but I always check what rate takes over after the intro period ends.

- Cash Advance APR: If I use my credit card to get cash from an ATM, the cash advance APR applies. This is usually higher than the purchase APR, and there’s no grace period. Interest starts right away.

- Penalty APR: If I miss a payment or pay late, the card issuer may apply a penalty APR. This rate is often much higher than my standard APR and can stick around for several months.

Variable vs. Fixed APRs and the Prime Rate

Credit cards generally have either variable or fixed APRs. Most cards issued today use variable APRs, which means the rate can change over time. The variable APR is usually tied to a financial benchmark called the Prime Rate. When the Prime Rate goes up or down, my card’s APR usually moves by the same amount. This makes my interest costs less predictable, but keeps them roughly in line with popular market conditions.

Some cards offer a fixed APR, so the rate stays the same unless the issuer gives me notice. Fixed APRs provide more stability, but they are rare nowadays and can still change under certain circumstances, usually with advance notice from the bank.

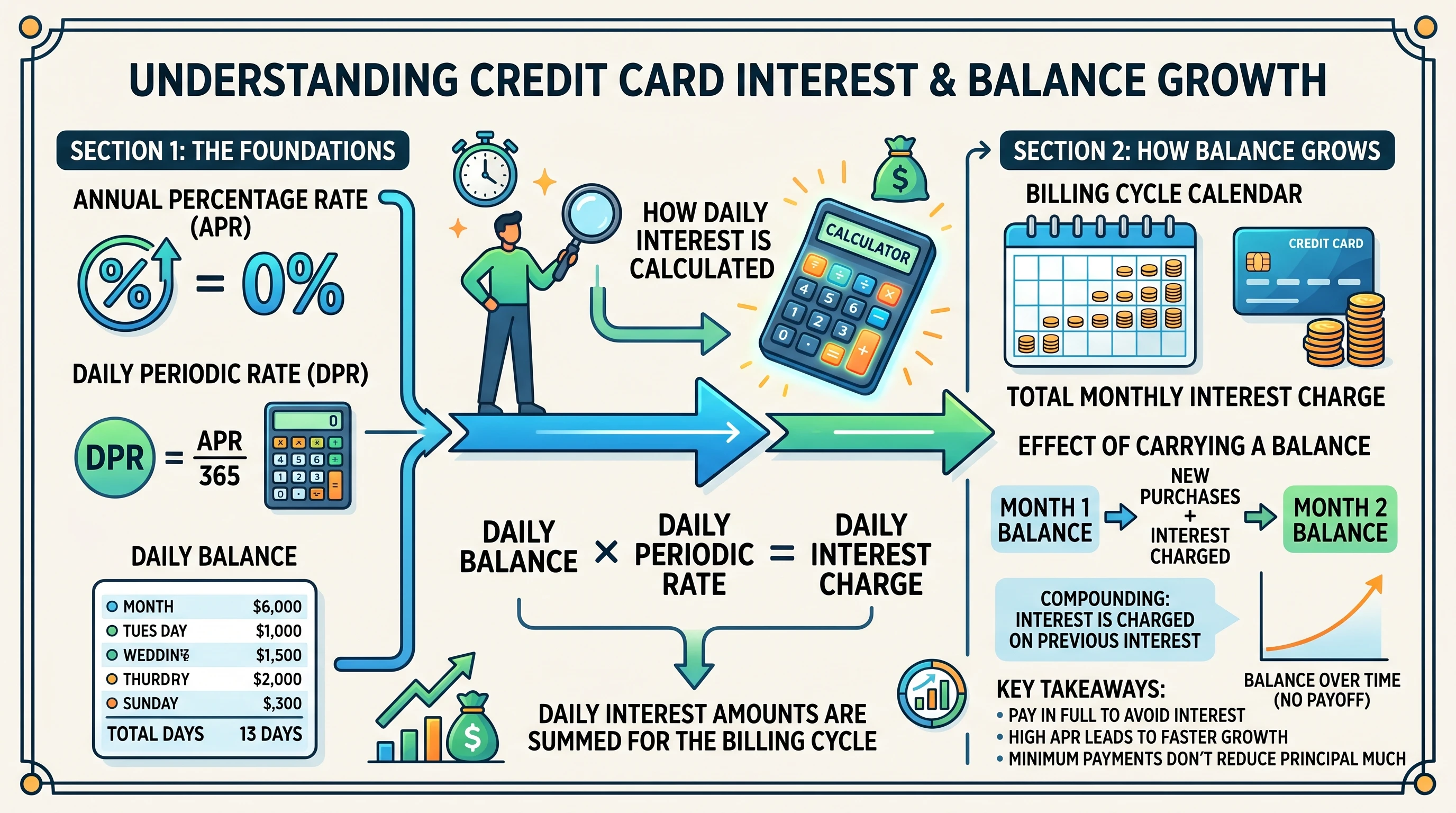

How Interest Is Calculated: Daily Rate and Average Daily Balance

Knowing how card companies actually calculate daily interest has helped me avoid unnecessary charges. Credit card issuers typically use a method called the Daily Periodic Rate (DPR). To get this, they take my yearly APR and divide it by 365 days. This becomes the rate charged on my balance each day I owe money.

The average daily balance method is common. The card company totals my balance for each day in the billing cycle, then divides this sum by the number of days in the cycle. The DPR is applied to the average daily balance each day, with interest compounding daily. This can cause my overall costs to rise quickly if I’m not careful.

Even a small balance can grow faster than I expect because the interest piles up not just on my purchases but also on previous interest amounts. This is known as compound interest, and it’s a key reason why paying off balances promptly really matters.

The Grace Period: How to Avoid Paying Interest on Purchases

The grace period is the time between the end of a card’s billing cycle and the due date shown on my statement. If I pay my statement balance in full every month during this period, I don’t pay any interest on purchases. This has always been my main strategy to avoid interest payments. As soon as I carry a balance past the due date, I lose this benefit and begin accruing interest immediately on new purchases as well, until the account is paid in full again.

Compound Interest: How Balances Grow Faster Than Expected

Credit cards use compound interest, meaning the interest I owe is added to my balance, and then future interest charges are based on this new, higher amount. Over time, this snowball effect can make even small balances balloon much bigger. If I only pay the minimum payment, I’m often just covering that month’s interest instead of actually paying down what I originally borrowed. To really tackle debt, paying more than the minimum is essential. This approach helps the balance shrink steadily and saves money over time.

Minimum Payments and Why Debt Lingers for Years

When I check my credit card statement, I always check how much is needed for the “minimum payment”. Paying just this amount usually goes mostly toward interest and fees, and only a tiny piece actually chips away at my balance. That’s how people can end up staying in debt for years even if they’re not using their card for new purchases. Paying more than the minimum or, in my experience, paying the full amount is the best way to reduce interest costs and get out of debt faster.

Understanding When Interest Starts for Purchases, Cash Advances, and Balance Transfers

For most purchases, interest doesn’t start if I pay my statement in full by the due date thanks to the grace period. For cash advances, though, there’s no grace period. Interest starts the minute I take out the cash. The same thing often happens with balance transfers unless I have a special introductory offer. This makes cash advances an expensive way to access cash, and it’s something I avoid unless I have absolutely no other option. Being aware of these rules helps me stay clear of truly costly transactions.

Promotional 0% APR Offers and Their Pros and Cons

Some credit cards attract new customers with a promotional 0% APR offer. This means I pay no interest on purchases or balance transfers for a set period, often 12 to 21 months. These offers can help me pay off big purchases or move existing debt from a higher-interest card. However, as soon as the promotional period ends, any remaining balance will start accruing interest at the standard rate, which is generally much higher.

I always read the fine print on these offers. Missing a payment can void the promo, and some cards even apply retroactive interest if I don’t pay off the full transferred balance in time. That’s why I set up reminders and track important dates so I don’t miss a deadline.

Factors That Determine My APR

Not everyone gets offered the same APR. My interest rate is influenced by several factors, including:

- My credit score; higher scores often mean lower APRs.

- My payment history; if I’ve paid late before, I might get a higher rate.

- My total income and my debt to income ratio; issuers want to see I can pay them back.

- General market interest rates; when the Federal Reserve raises or lowers rates, credit card APRs usually change too.

Checking these factors before applying for a new credit card helps me shop around for a better deal, and it motivates me to keep my credit score healthy by paying my bills on time and limiting my debt. Knowing what impacts my rate helps me make smarter choices.

Statement Balance vs. Current Balance

When I view my credit card account online, I usually see two balances: the statement balance and the current balance. The statement balance is what I owe at the end of the billing cycle. Paying this in full by the due date lets me avoid interest on purchases. The current balance includes recent purchases made after the statement closed. If I pay the current balance, I’m always ahead. However, paying at least the statement balance on time is enough to avoid interest on new purchases, so I make sure to keep those deadlines.

Paying Early and Making Multiple Payments: Reducing Interest

Paying off my purchases early, or making multiple payments throughout the month, has helped me reduce my average daily balance. Since issuers calculate interest based on my daily balances, every dollar I pay off early means less money that accrues interest. This strategy is especially helpful if I’m carrying a balance or using a card without a grace period, and it’s a trick that can shave dollars off my bill over time.

Strategies for Minimizing Credit Card Interest

- Pay my statement balance in full every month to avoid interest charges.

- If I can’t, pay more than the minimum to pay off the balance faster.

- Stay away from cash advances, which accrue interest immediately and often come with extra fees.

- Use promotional 0% APR offers to my advantage, but always check dates and rules.

- Work on improving my credit score and history to qualify for lower rates.

On top of that, I keep an eye on my billing cycles and try to automate payments to avoid missed due dates. Being proactive with payments makes a noticeable difference in my financial health over time.

Common Credit Card Fees I Watch Out For

Besides interest, card companies may charge extra fees. Here’s what I look out for:

- Annual fee: Charged once a year, especially on cards with rewards or special perks.

- Late payment fee: Charged if I miss a payment due date.

- Balance transfer fee: Commonly 3%–5% of the amount transferred from another card.

- Cash advance fee: Usually a percentage of the amount withdrawn, plus interest from day one.

- Foreign transaction fee: A fee on purchases made outside my country, often 2% to 3%.

- Returned payment fee: Charged if a payment fails, like a bounced check.

Reviewing my card’s terms gives me a full picture of what I may be charged for different types of transactions. Sometimes, picking a card with fewer fees is worth more than a small rewards program or other perks.

Best Practices for Managing Credit Card Interest

Based on everything I’ve learned, here are some habits I stick to for smart credit card use:

- Always pay on time, even if it’s just the minimum when money is really tight.

- Keep my credit utilization low; ideally under 30% of my credit limit for the highest credit score benefit.

- Check my statements regularly for accuracy and unexpected charges—quickly catching mistakes can save headaches down the road.

- Avoid carrying balances if I can help it. Credit cards work best as a payment tool, not a longterm loan.

- Use credit as a tool for convenience and rewards, not as a way to finance major purchases I can’t afford to pay off quickly.

I find that treating my card responsibly helps me avoid fees and expensive interest charges, and it helps build a solid credit history for the future. Also, exploring educational resources about credit cards has helped me make smarter decisions, so I keep learning whenever I can.

For even more information on how to pay off outstanding debt, check out our full article on debt reduction tips and tactics here.

Have questions or want to share your own experiences with credit card interest? Drop a comment below. I’m always interested to hear how others manage their cards!